Education Loan vs Self-Funding: What Indian Students Must Know Before Studying Abroad

Planning studying abroad is not just an academic decision — it is a major financial commitment. One of the most important questions Indian students and parents face is:

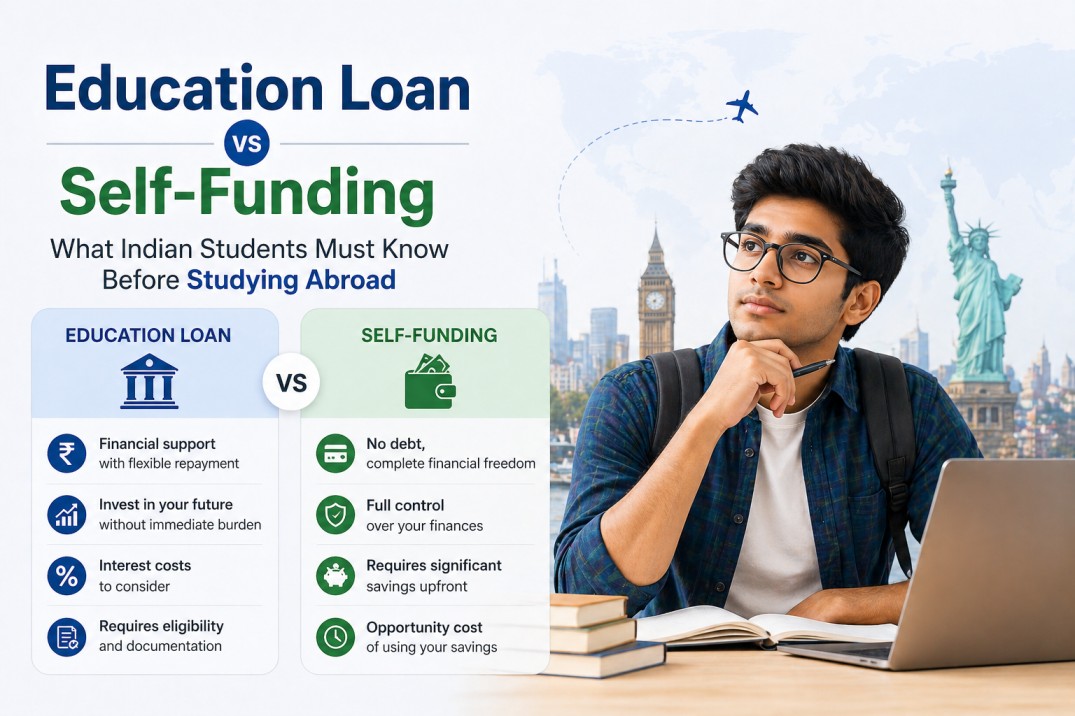

Should you take an education loan for study abroad or use self-funding?

Both options have advantages and risks. Choosing the wrong approach can lead to financial strain, delayed payments, or even visa complications. A structured financial decision helps students manage costs effectively and focus on their education.

This guide explains Education Loan vs Self-Funding in a practical, transparent way so students can decide how to finance foreign education responsibly.

Education Loan vs Self-Funding – Making the Right Financial Decision

Before comparing both options, students must understand the full cost of international education. Many families underestimate expenses by considering only tuition fees.

A complete financial plan should include:

- Tuition fees

- Living expenses

- Accommodation

- Health insurance

- Visa and immigration costs

- Travel expenses

- Emergency funds

Whether you choose education loans or self-funding, planning for total cost is essential.

Tuition & Living Cost Reality

The cost of studying abroad varies by country and university. However, students should always calculate the total annual expense instead of only tuition.

Example Cost Range (Approximate)

USA

₹25 – ₹55 lakhs per year

UK

₹20 – ₹40 lakhs per year

Canada

₹18 – ₹35 lakhs per year

Australia

₹20 – ₹40 lakhs per year

Dubai

₹12 – ₹20 lakhs per year

These figures include both tuition and living expenses.

Students who rely entirely on savings must ensure they can fund the entire course duration, not just the first year.

Self-Funding: Advantages and Considerations

Self-funding means financing your education using personal savings, family funds, or assets.

Advantages

- No loan repayment burden

- No interest costs

- Faster visa documentation in some cases

- Financial independence after graduation

Considerations

- Large upfront financial commitment

- Savings depletion risk

- Limited emergency buffer

- Reduced liquidity for families

Self-funding works best for families with strong financial reserves and stable income sources.

Education Loan for Study Abroad: Advantages and Considerations

Many students use education loans to finance foreign education. Loans allow families to distribute financial pressure over time instead of paying everything upfront.

Advantages

- Reduced immediate financial burden

- Structured repayment after graduation

- Preserves family savings

- Helps fund higher-ranked universities

Considerations

- Interest accumulation

- Repayment responsibility

- Loan eligibility criteria

- Collateral requirements (in some cases)

Education loans can be a strategic option when managed responsibly.

Collateral vs Non-Collateral Loans

Education loans are typically categorized into collateral-based and non-collateral loans.

Collateral-Based Loans

These require security such as:

- Property

- Fixed deposits

- Other assets

Advantages:

- Lower interest rates

- Higher loan amounts

- Flexible repayment options

Considerations:

- Asset pledge requirement

- Processing time may be longer

Non-Collateral Loans

These do not require asset security.

Approval depends on:

- Academic profile

- University ranking

- Co-applicant income

- Course relevance

Advantages:

- No asset pledge

- Faster processing

Considerations:

- Higher interest rates

- Lower loan amounts

Understanding study abroad loan eligibility helps students choose the right loan type.

Interest Rates & Moratorium

Interest rates vary based on:

- Loan amount

- Collateral availability

- University ranking

- Course type

Most education loans offer a moratorium period, which includes:

- Course duration

- Additional grace period after graduation

During this period:

- Some loans allow no payments

- Some require interest servicing

Students must understand the repayment structure before applying.

Risks of Underestimating Costs

One of the biggest mistakes students make is underestimating expenses.

Common oversights include:

- Currency fluctuations

- Accommodation price increase

- Health insurance costs

- Travel and relocation expenses

- Emergency funds

If funding falls short, students may face:

- Payment delays

- Visa complications

- Academic disruption

A realistic financial plan prevents these risks.

When Self-Funding Makes More Sense

Self-funding may be suitable if:

- You have sufficient savings

- You prefer no debt

- Course cost is moderate

- Family income is stable

This option offers peace of mind but requires strong financial discipline.

When Education Loan Is a Better Option

Education loans may be suitable if:

- You want to preserve savings

- You aim for high-ranked universities

- Course offers strong career outcomes

- You prefer structured repayment

Loans can help students access better academic opportunities without financial pressure.

Hybrid Approach: A Balanced Strategy

Many families use a combination of:

- Partial self-funding

- Partial education loan

This approach:

- Reduces loan burden

- Preserves savings

- Improves financial flexibility

Hybrid funding is often the most practical solution.

Role of Professional Loan Assistance

Applying for education loans requires:

- University selection alignment

- Financial documentation

- Co-applicant evaluation

- Loan eligibility assessment

Professional financial planning for studying abroad helps students:

- Compare lenders

- Choose loan type

- Understand repayment terms

- Prepare documentation

Guidance reduces delays and improves approval chances.

Final Thoughts

Choosing between education loans vs. self-funding depends on your:

- Financial capability

- Risk tolerance

- Career goals

- Course cost

- University selection

There is no universal right answer. The best decision is the one that balances affordability with long-term career growth.

Students should always evaluate how to finance foreign education carefully before applying.

Need Help Planning Your Study Abroad Finances?

Before selecting funding options, evaluate your total education cost and loan eligibility.

Study Metro provides structured guidance on:

- Education loan options

- Financial documentation

- Funding strategy

- Budget planning

Speak to our education loan advisors before applying and plan your international education with clarity.

👉 Read next: Why Professional Study Abroad Counseling Increases Admission Success Rates

Understand how expert guidance helps with university shortlisting, SOP preparation, documentation, and visa readiness—improving your chances of securing admission.